Record-breaking post-Holiday sales masked a marked slowdown in overall retail spending. Despite Black Friday and Cyber Monday sales surpassing $20 billion for the first time in history, U.S. retail spending experienced its most significant decline of the year, suggesting households are making strategic financial decisions as they plan for the road ahead. The economy remains at an unprecedented crossroads, with many questions looming:

Will inflation continue to slow, and how much further could interest rates rise? The Fed continues to raise rates at a slightly slower pace and has signaled its intention to continue doing so at least through the spring.

Will a slightly slowing economy morph into a full-blown recession, and will the labor market remain strong? While sales and margins show signs of softening, the labor market continues to defy expectations, making it hard for the Federal Reserve to further ease the policy. Layoffs in the technology, media and real estate industries make headlines. Still, they represent a minuscule portion of the labor force, with overall jobless claims falling by 20,000.

How much longer will pandemic-era savings and easing supply chains buttress consumer spending, and will they continue to spend more on necessities? While personal savings soared to nearly $6.5 trillion in 2020, they’ve since dropped to below $500 billion, lower than the $1.4 trillion pre-pandemic. Despite supply chain imbalances driving discount sales as retailers looked to shed excess inventory, consumers are focusing their budgets on food and other staples and spending less on holiday categories such as electronics, clothing, and sporting goods.

Ultimately, is a recession inevitable, and how bad might it get? This remains anyone’s prediction, but for business owners, management teams, and industry leaders, any level of uncertainty should be met head-on – waiting to seek clarity can be a losing move.

Connect with G2 to discuss your 2023 strategic objectives. At G2 Capital Advisors, deep sector and operational expertise underscore our dedication to achieving success at all costs. We support clients through both healthy market cycles and times of distress, with a refusal to fail. We provide highly tailored advice to company-specific circumstances in an ever-changing world. Reach out today to start the conversation.

G2 has had an exceptional start to the year, actively supporting over 95 engagements across four industries, serving investment banking and restructuring clients. The firm has made significant investments to expand our leadership functions across the organization with the addition of:

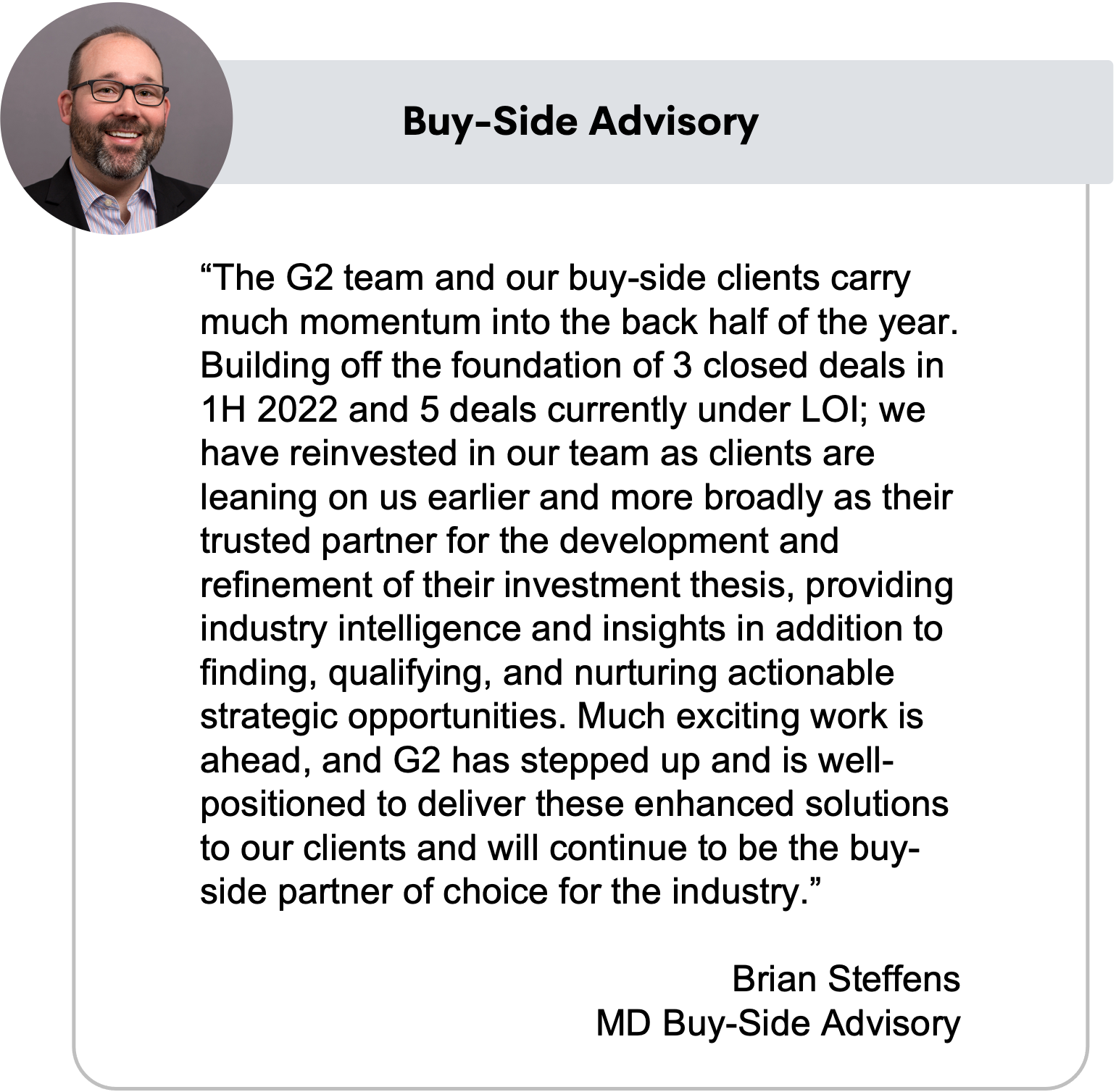

- Brian Steffens – Managing Director, Buy-Side Advisory

- Brian Schofield – Managing Director, Head of Capital Markets

- Jim Cotter – Managing Director, Industrials & Manufacturing

- Jereme LeBlanc – Director, Buy-Side Advisory

As we carry our momentum to the back half of 2022, G2 maintains a steadfast commitment to meeting the evolving needs of our clients across all stages of the business lifecycle. Whether executing strategic growth through M&A or supporting businesses troubled by unsustainable capital structures or challenging industry or operating conditions, G2 is your partner from beginning to end.

CLOSED TRANSACTIONS:

|  |  |  |

|  |  |  |

|

NOTABLE ENGAGEMENTS:

|  |  |  |

|  |  |  |

PERSPECTIVES FROM LEADERSHIP

|  |

|  |

|  |

|  |

Corporate life often mirrors personal experiences. The COVID-19 pandemic shook the foundations of our lives, prompting a series of unexpected consequences across both our personal and professional domains. At the onset of the pandemic, most people did not anticipate such a significant disruption that would last well over a year. Some have gained the “freshman 15 pounds” during quarantine due to limited mobility, lack of exercise, and extended periods in front of computer screens on zoom calls in sweatpants all day. And there are those who took the opportunity to refocus, establish discipline in their routine, and get in the prime shape of their life. This analogy can be applied to the corporate world as well. Leaning up your organization will remain critically important in this uncertain future.

CLIENT:

Arbre Group Holding Corporation (“AGH”) is a family-owned business that began in 2009 following the acquisition of the assets of Arbre Farms Corporation (“AFC”) and Willow Cold Storage Corporation (“WCS”, together with AFC, “the Company”). AGH has roots dating back to 1948 when Francis Marks founded a fresh produce company. Through its wholly owned subsidiaries, including Paris Foods Corporation, Holli-Pac Inc. and Sun Mark Foods, AGH offers processing, re-packaging, distribution, and storage for a variety of frozen fruit and vegetable products.

SITUATION:

AGH was formed through a combination of frozen fruit and vegetable processing, re-packaging, cold storage, and distribution businesses across Central and Eastern U.S. G2 Capital Advisors, LLC (“G2”) was initially engaged by the Board of Directors of AGH to evaluate strategic alternatives for the Company in service of helping them realize their long-term vision, including a current state analysis of the business, assessment of potential growth opportunities and development of financial and operational alternatives. Following thoughtful consideration of the strategic alternatives, the Board of Directors engaged G2 to pursue partnership opportunities for its processing assets, allowing AGH to allocate resources to its core distribution businesses.

ENGAGEMENT:

G2 served as the exclusive financial advisor to AGH, leading an expedited, hands on process to evaluate partnership opportunities for AFC and WCS. G2 focused on identifying potential partners for the Company with deep operational expertise in food processing and who understand the value of the facility and assembled assets.

“The AGH team trusted G2 to run the process to support its long-term vision for its companies. It was a pleasure working with the AGH team to deliver the optimal outcome for AFC and WCS. We are excited about the future and look forward to watching the continued success of the Company with a highly capable partner in OPC.” said Don Van der Wiel, Managing Director for G2.

OUTCOME:

After evaluating various partnership options, AGH determined a carve out sale of the Company ultimately presented the best path forward for AFC and WCS. The transaction was successfully closed on April 30th, 2021 through a sale of AFC and WCS to Oregon Potato Company (“OPC”), and assigned to OPC Arbre Farms, LLC. The acquisition strengthens OPC’s position as a leader in the vegetable processing and distribution space to better serve its customers across North America.

“This outcome provides AFC and WCS with an opportunity to leverage OPC’s footprint, expertise, and relationships to accelerate growth and extend its reach in the frozen vegetable market. We thank G2 Capital Advisors for guiding us through this complex and detailed process. G2 acted as an extension of our team providing valued support and trusted advice throughout.” said Dylan Marks, President & CEO of AGH.

About Arbre Group Holdings:

Founded in 2009 with history dating back to the late 1940’s, AGH through its subsidiaries specializes in globally sourced frozen fruit and vegetable wholesale distribution, frozen produce importing, frozen vegetable processing, frozen produce re-packing, and cold storage services to the retail grocery, foodservice, and frozen food manufacturing companies throughout North America.

About G2 Capital Advisors:

G2 Capital Advisors provides M&A, capital markets and restructuring advisory services to the middle market. We offer integrated, multi-product and sector-focused services by pairing highly experienced C-level executives with specialist investment bankers. We aspire to be the trusted advisor of choice to our clients including corporations and institutional investors.

CONTACTS ON THIS DEAL:

Ben Wright, COO: E: [email protected]

Don Van der Wiel, Managing Director: E: [email protected]

Zach Talotta, Senior Associate: E: [email protected]

Kevin Lamb, Senior Analyst: E: [email protected]

Andrew Keleher, Vice President: E: [email protected]

G2’s unique team of seasoned C-level executives, restructuring advisors and investment bankers provide our clients with a clear path to long term operational stability, a sustainable capital structure, and the financial flexibility necessary to achieve their strategic goals. G2 generates substantial value for stakeholders through our operational and transactional capabilities and focus on risk mitigation.

“This recession will finally end the private-sector ‘debt super-cycle,’ says firm that invented the term” – MarketWatch, April 4th, 2020

Over the past decade, forecasters have been anxiously tracking rising corporate leverage levels and the proliferation of covenant-light loans, while lamenting the woefully declining credit quality of borrowers. Lenders could only “amend and pretend” for so long, they argued, and it would be just a matter of time before we witnessed an apocalyptic deleveraging event that would finally mark the end the current debt cycle. The sovereign debt crisis, tariff war, inverted yield curve, all came and went, but a global pandemic should have been the final straw. As infections and lockdowns spread in early 2020, commentators competed to see who could predict the biggest surge of bankruptcies and corporate defaults.

By Q3 defaults had fallen to below pre-COVID levels, and yields had declined dramatically across the board. In a shocking turn of events, debt issuance had surged to record levels, providing liquidity to healthy and distressed borrowers alike. The ultimate irony was, as S&P Global noted, investors “were so supportive that some of the corporate sectors that saw the largest increases in bond issuance relative to the prior five years were those most negatively affected by economic lockdowns.” Undeterred, commentators have now rolled forward their doomsday forecasts, bracing for an even bigger deleveraging and fallout in 2021. But what if we have collectively “broken” the corporate debt cycle? Consider the following three factors:

First, and foremost, is the Fed backstop, which involved unprecedented direct lending to both investment grade and distressed borrowers. Overnight, the Fed’s balance sheet nearly doubled to $7.4 trillion, all but ensuring that the Fed will be a permanent participant in private credit markets. Markets are inarguably in “risk on” mode, and it’s difficult to imagine any kind of crisis of confidence in the foreseeable future.

Second is the near-mythical “search for yield” and its side-effects, specifically the prolific rise of non-bank lending. Institutional investors, grappling with falling returns on fixed income and other assets, have pushed deeper into the private credit market. AUM at private debt funds has skyrocketed from under $200B in 2007 to nearly $900B, with $300B of dry powder waiting to be deployed. The new breed of lenders is more creative and better-equipped than traditional banks at segmenting and capturing risk premium at all levels of the capital structure. These investors, willing to take greater risks, were happy to put money to work during the pandemic, while banks battened down the hatches and sat on the sidelines. For these lenders, COVID has become a mere EBITDA adjustment, and most were willing to ride out the storm and “amend and extend” into 2021 leaving the search for yield poised to continue unabated into the future.

Last, but not least, is the evolution of lenders’ strategic options for dealing with distressed loans. Historically, a bank loan workout was a lengthy affair, with a forbearance or amendment followed by a two or three-year operational turnaround of the borrower. Today’s lenders prefer to move quickly to exercise their remedies. They are frequently turning to secondary debt sales, special-situation refinancings, carveouts or expedited sales of the company. Increased specialization means that there are buyers for every type of security, asset, and distressed business or division. For deeply troubled credits, options such as Article 9 foreclosures or Section 363 sales can be used as a tool to efficiently foreclose and sell viable assets at premium prices, and then wind down the remaining liabilities through either an in- or out-of-court process. As a top-tier middle market restructuring advisor, we employ these strategies (and more) every day on behalf of our clients, and have witnessed firsthand how lenders can now dynamically shift risks throughout this ecosystem. More and more, lenders rely on our firm to provide not only financial and operational support, but also integrated banking capabilities and increasingly advanced legal sophistication.

In sum, we could be witnessing the end of the broad-based credit cycle, and the start of a new era characterized by more complex, localized pockets of risk accompanied by fewer, but larger, distressed events. The current debt-cycle may live on for some time yet.

Konstantin A. Danilov is a Vice President at G2 Capital Advisors, which provides M&A, capital markets and restructuring advisory services to the middle market.

G2 Capital Advisors, LLC (“G2”), a leading full-service financial advisory firm, is pleased to announce that Christopher Capers has joined the firm as Managing Director within the Restructuring practice, with a focus on operational turnarounds. He will be located in the Southeast and reporting to Ben Wright, COO as he continues the growth & expansion of G2’s presence in the Southeast region. Christopher brings over 25 years of experience across executive leadership roles in corporate and entrepreneurial environments supporting healthy and stressed businesses. This appointment reflects G2’s continued investment in providing unparalleled operational capabilities to revitalize clients.

“Christopher’s extensive leadership experience enhances G2’s differentiated advisory approach, while also deepening our value creation proficiency in the industrials and manufacturing sector.” said Ben Wright, Chief Operating Officer of G2 Capital Advisors.

Christopher has specialized in operational restructuring and turnarounds through his comprehensive consulting and hands-on operational experience. Christopher has provided expert advisory guidance to companies requiring revitalization, including improving product profitability, reducing costs, managing pricing, building lean manufacturing, enhancing asset utilization, refining sourcing, and enhancing supply chains.

Before joining G2, Christopher was a senior Executive with Novolex Packaging, where he was Head of Operations Strategy and Continuous Improvement across a global manufacturing network. He championed operational excellence and lean manufacturing techniques to drive performance efficiency, establish manufacturing standards, and institute operational savings. In addition, he was responsible for warehouse distribution consolidation and M&A integration.

Prior to Novolex, Christopher served as a C-level Executive for multiple growth stage entrepreneurial ventures and a Director at AlixPartners Restructuring, leading value creation initiatives for private equity clients and various corporations in distressed or bankruptcy environments. Additionally, Christopher brings over a decade of experience in operational consulting with Booz Allen Hamilton.

“We are excited to welcome Christopher to the G2 team,” said Jeffrey Unger, Chairman & CEO of G2 Capital Advisors. “We continue to drive rapid growth across the G2 platform through this unique market environment. Christopher, as a Managing Director within Restructuring, will be a critical driver of our continued success as we enter 2021.”

Christopher holds a Master of Business Administration from Harvard Business School and a Bachelor of Science in Mechanical Engineering from the University of Pittsburgh.

What is Assignments for the Benefit of Creditors?

Also known as “ABCs”, Assignments for the Benefit of Creditors is a solution for troubled companies and a key part of G2’s fiduciary services along with bankruptcy advisory and out-of-court wind-down management. As inflation and increasing interest rates blunt business activity, more and more distressed companies will be evaluating their options. If pursuit of lifeline capital or a trade sale exit doesn’t materialize for a company facing creditor uproar and a finite cash runway, winding down may be the unpleasant but necessary next step. Privately held companies in this difficult position should weigh the merits of various paths forward with guidance from trusted advisors

An “ABC” is a corporate liquidation process available to an insolvent company that has run out of options. A nimble procedure governed by state statute rather than federal law, ABCs are often an attractive alternative to bankruptcy and other options since they are usually faster, simpler, less expensive, and yield better outcomes. While not suitable for all situations (e.g., a company with highly complex multi-state operations and litigious creditors), an ABC is a recognized proceeding that a board can avail itself of to maximize recovery for creditors and minimize its liability. ABCs have grown in popularity in recent years with venture-backed technology companies and traditional brick-and-mortar firms alike.

Some examples when you might want to consider an ABC to liquidate a company’s assets and pay off creditors:

- Insolvency: When you are unable to make due dates on payments and bills for your company.

- Lack of Funding: If a company is struggling to secure additional funding to ensure the continued success of business operations.

- Legal Disputes: If a company is undergoing legal suits that may pose a threat to its financial stability.

Whether an ABC is the right option for a business depends on a multitude of circumstances and each situation is unique. It’s important to seek financial advice before making any decisions. To learn more about G2’s capabilities and get in touch, contact us today.

Pros and Cons for Each Type of ABC Option:

- An informal wind-down and dissolution is straightforward but likely not feasible if remaining cash is insufficient to pay back creditors.

- A Chapter 11 bankruptcy is a formal reorganization process that plays out in court. Often the best route for companies that have substantial operations and face the threat of heavy litigation, this proceeding rarely makes sense for a small company. It is expensive, public, requires court filings and approval for major actions, and takes at a minimum several months to complete.

- In a Chapter 7 bankruptcy, which is likewise expensive, a court-appointed trustee administers the asset liquidation. Trustees often lack industry knowledge, incentives to act with urgency, and the ability to operate the business, should doing so for a short period benefit creditors.

- A foreclosure sale under UCC Article 9, while quicker and cheaper than bankruptcy, may not yield optimal value for the assets, and requires that the lender take responsibility for the sale effort—which they may not have the resources, expertise, or desire to doHere’s how it works: with consent from its board and shareholders, a distressed company transfers ownership of its assets (technology, inventory, machinery, etc.) to a third-party fiduciary of its choosing—the “Assignee”—through a general assignment agreement. The Assignee then sells the assets in an accelerated timeframe, communicates with stakeholders, distributes remaining cash to creditors, and manages the administrative wind-down of the Company.

What are the steps to an Assignment for the Benefit of Creditors?

With consent from its board and shareholders, a distressed company transfers ownership of its assets (technology, inventory, machinery, etc.) to a third-party fiduciary of its choosing—the “Assignee”—through a general assignment agreement.

The Assignee then sells the assets in an accelerated time frame, communicates with stakeholders, distributes remaining cash to creditors, and manages the administrative wind-down of the Company. While providing the company’s board members and officers with many of the protections of a bankruptcy proceeding, an ABC can be made at a fraction of the cost. ABCs happen without judicial oversight in key states (California, Massachusetts, Illinois, etc.), enabling Assignees to move quickly. A speedy process maximizes creditors’ recovery, since many acquirers want to pursue, in parallel with their purchase of the assets, a company’s customers and key employees as well—who would likely be off the market if the process were to take too long. The Assignee is able to continue to operate the business, as long as those operations are financially solvent.

Exploring an ABC makes sense when it becomes clear the runway is limited. If the business will be unable to remain a going concern without the closing of a company sale transaction or capital infusion, contingency planning around wind-down options, including ABCs, is prudent.

When a company approaches insolvency (inability to pay debts as they come due) the board must act with caution since creditors replace shareholders as the primary beneficiaries of any residual value of the business. Directors of an insolvent corporation are exposed to claims from creditors that the directors’ actions harmed enterprise value and thus failed to protect creditors’ interests. If future prospects are limited and ongoing operations would deepen financial troubles, an ABC can be a graceful way to exit and should be considered.

Who benefits in an ABC?

- The creditors – since an experienced Assignee is officially working to maximize their recovery. The Assignee can take the assets to market immediately upon ABC launch (as opposed to the three-to-six-week delay in a Chapter 7 bankruptcy), and engage company personnel to assist, thus preserving asset value and institutional knowledge.

- The board – since they can minimize their liability by resigning day one of the ABC, and do not face the disclosure requirements (and therefore stigma) of a bankruptcy.

- The acquirer – since the assets are sold free and clear of liens and related liabilities, and the sale can close quickly—without the need to obtain court approval (in many states).

- The company’s vendors and customers – since they can start a fresh relationship with the (presumably solvent) asset buyer.

How G2 Can Help

As a premier financial advisory boutique, G2 Capital Advisors helps troubled companies evaluate available options, gain stakeholder buy-in, and implement the best solution. G2’s experience with ABCs and other fiduciary services covers an array of industry sectors and geographies. Before an ABC, G2 communicates with clients to explore the situation, identify the best options while keeping in mind costs. From there, we will help decide a plan for success and whether an ABC makes sense for said company.

Our investment banking prowess ensures a professional asset sale process that will yield the highest possible recovery for creditors. G2’s capabilities in special situations span the full range of operational and financial restructuring options available to distressed middle market companies. As an effective tool for both satisfying creditors and allowing stakeholders to exit, an ABC is one such option that a company facing crumbling business prospects may want to consider.

Nate McOmber

Managing Director

415-825-5866

[email protected]

As we enter the typical fall budgeting process, G2 has been assisting our clients in exploring new ways to approach 2021 forecasting given the uncertainty related to the COVID-19 pandemic and its impact on various industries over the near to medium term. Many operators and their finance teams are struggling to reliably forecast their businesses, making strategic planning more challenging and limiting stakeholders’ ability to assess the long-term prospects for their companies. Through our financial advisory and turnaround consulting engagements, G2 has been leveraging a number of key practices to enhance the productivity of 2021 budget building, helping companies and their management teams plan proactively manage the uncertainty:

• Consider New Methodologies

o Year-over-year variance modeling – When a business has seen temporary pandemic related demand disruptions, we’ve applied efficient top down discounts to 2019 actuals or 2020 original budgets to drive revenue assumptions for 2021. The top down discounts can be refreshed based on latest views on the depth and duration of the impact of the pandemic on a particular business or industry. By layering on updated cost structure assumptions based on management’s various initiatives, a full profitability picture can take shape. For indoor businesses, like restaurants or retailers, G2 has been similarly modeling the revenue impact of the pandemic through the winter months in colder geographies in the U.S.

o Bottoms up around the “New Normal” – For companies with significant and likely permanent changes to their operating realties, a bottoms up full budgeting process may be the preferred method. Benefits include revisiting detailed revenue assumptions, which can prompt creative approaches or calls to action to drive new revenue opportunities. Similarly, divisional level, line item by line item review of cost structures can yield material expense reduction opportunities or nimbler, potentially tech enabled operating models explored during the pandemic.

o Build multiple “cases” vs. one baseline budget – Clients that severe pandemic related revenue declines have typically taken a scenario modeling approach to budgeting, focusing more on potential states of the world and the associated impact on the business, rather than on presenting one budget, that with certainty will be wrong.

• Scenarios modeling is more valuable than ever

We value “sensitizing” forecasts based on key assumptions and drivers in order to stress test profitability and liquidity in times of significant uncertainty. By creating upside (vaccine in Q1) and downside cases (no vaccine), leadership teams arm themselves with key insights on the range of potential outcomes for both revenue and expense level recoveries. Furthermore, stress tests provide clients with insight into what breaks the business and how to proactively manage cost structures and liquidity (keeping dry powder for CAPEX or working capital investments) based on topline trends and other key indicators of business activity. Commodity costs can be a key driver of margins and warrant particular scrutiny in scenario models. Stress testing covenants and minimum available liquidity is critical in leveraging forecasts as a tool to provide transparency and peace of mind to lenders at this time. Consider also pulling forward the budgeting process timeline in order to get estimates of potential outcomes in 2021 earlier, allowing management to take more aggressive action sooner.

• Flexibility may be more valuable than granularity

In times of high uncertainty, building granular bottoms up forecasts require significant resources and provide limited value given the pace of change. The return on those resources can be enhanced by building flexible models that can be updated over the course of the year with actuals and refreshed on a rolling basis. A dynamic forecast is highly valuable in providing leadership with real time forward views and empowers nimbler responses on driving revenue opportunities and trade-offs on investment, especially in a recovery scenario where working capital requirements can be significant.

• Bridge Building

We recommend tracking the impact of COVID-19 on revenue, costs, and cash in order to bridge between 2020 actuals to a pro forma, adjusted view of the business. Analyzing 2021 forecasts and scenario cases through EBITDA or free cash flow bridges isolates key assumptions and plays a critical role in educating stakeholders on drivers of performance. For more challenged situations, sizing cash needs becomes a critical output of the 2021 budgeting process, whether funding operating losses or working capital. Solving for these liquidity needs in the form of a “cash bridge” has been a key focus across many G2 engagements with pandemic impacted companies.

G2’s highly capable team, including seasoned interim CFOs, Controllers, or FP&A resources, not only can help our clients navigate challenging liquidity or performance environments, but also can drive improvement in core finance/accounting functions. Feel free to reach out to the G2 team to learn more about the approaches we are using across our 45 plus clients in our industries of focus.

CLIENT

Directed, LLC (“Directed”), is a Vista, California-based producer of automotive aftermarket electronics. Directed, a world leader in automotive electronics, is the largest North American designer and marketer of consumer-branded vehicle security and remote start systems, and a pioneer in the connected car space. Its products connect more consumers to their vehicles than anyone else on the planet. Directed markets its broad portfolio (sold under Viper®, Clifford®, Python®, Autostart®, AstroStart®, Alcohol Detection Systems® and other brands) through leading national retailers and specialty chains.

SITUATION

In March, Directed experienced significant operational and cash flow challenges due to the impact of the global COVID-19 pandemic. It’s customers, who represent leading national automotive after-market retailers and specialty chains, experienced a significant decline in store traffic and related consumer spending, especially on account of actions taken in response to the public health crisis. Mandated store closures significantly contributed to missed sales targets and resulted in unsold inventory.

ENGAGEMENT

Faced with a liquidity crisis, Directed engaged G2 Capital Advisors, LLC (“G2”) as its restructuring advisor. Directed’s board of directors tapped G2 Managing Director Jeffrey T. Varsalone to serve as Directed’s Chief Restructuring Officer (“CRO”). Through the CRO, G2 developed and executed liquidity management tactics to maximize runway for a potential restructuring transaction and assessed strategic options for the Company and its stakeholders. With a focus on maximizing value for creditors and preserving jobs, G2 provided the board with restructuring expertise in negotiating a consensual resolution with the Company’s lender and facilitating a restructuring transaction that preserved the going concern. G2 teamed with Livingstone Partners, LLC, which ran an expedited sale process as the Company’s investment banker.

OUTCOMES

Implementing tight liquidity management measures, G2 assisted Directed in negotiating a series of forbearance agreements without creating additional exposure for the Company’s senior lender. As a result of the ability to avoid incremental risk to the senior lender, the Company had sufficient runway to consummate two asset sale transactions in July 2020 that preserved the value of the going concern. The first was the sale of Directed’s Remote Start & Security and Connected Car Solutions businesses to VOXX International Corporation (NASDAQ: VOXX), a leading manufacturer and distributor of automotive and consumer technologies for the global markets. The second was the sale of Directed’s ignition interlock device business, Alcohol Detection Systems (“ADS”), to CST Holding Company (“CST”). CST is a portfolio company of private equity firm Welsh, Carson, Anderson & Stowe (“WCAS”) and also owns the nation’s largest ignition interlock brand, Intoxalock.

“Having assessed the limited potential recovery to stakeholders in a liquidation scenario, this was a particularly challenging situation,” said Jeffrey T. Varsalone, the Company’s Chief Restructuring Officer. “The uncertainty of being able to consummate a going concern sale transaction during the height of the Covid lockdown this spring created a dynamic where the runway had to be created without asking stakeholders to take on material additional risk. The board, the Company’s management and the Company’s professionals worked together tirelessly and cohesively to maximize value for all stakeholders. We are very proud to be part of the team that provided value to creditors, provided an ongoing customer to vendors, and saved over 100 jobs at a time when the annualized unemployment rate was at an all-time high”, Varsalone concluded.

Joseph Greenwood and Andrew Bozzelli from Livingstone led the investment banking effort in selling Directed. L. Katherine Good, Esq. and Michael W. Whittaker, Esq. of Potter Anderson & Corroon LLP served as legal counsel to Directed.

This transaction is part of several recent G2 transactions, including The Paper Store, LLC (CRO engagement culminating in Chapter 11 Section 363 Sale) and a regional casual dining restaurant chain (CRO engagement culminating in a sale transaction).

About Directed:

Headquartered in Southern California, Directed is the largest designer and marketer in North America of consumer-branded vehicle security and remote start systems (sold under Viper®, Clifford®, Python®, Autostart® and other brand names). Directed markets its broad portfolio of products through many channels including leading national retailers and specialty chains throughout North America and around the world.

About VOXX International:

VOXX International Corporation (NASDAQ: VOXX) has grown into a leader in Automotive Electronics and Consumer Electronics, with emerging Biometrics technology to capitalize on the increased need for advanced security. Over the past several decades, with a portfolio of approximately 35 trusted brands, VOXX has built market-leading positions in in-vehicle entertainment, automotive security, reception products, a number of premium audio market segments, and more. VOXX is a global company, with an extensive distribution network that includes power retailers, mass merchandisers, 12-volt specialists and many of the world’s leading automotive manufacturers.

About Intoxalock:

Intoxalock, is the primary DBA of Consumer Safety Technology, LLC, is a leading provider of ignition interlock devices, which are breathalyzers installed in vehicles. Intoxalock is based in Des Moines, Iowa, United States. CST is a portfolio company of private equity firm Welsh, Carson, Anderson & Stowe.

About G2 Capital Advisors

G2 Capital Advisors provides M&A, capital markets and restructuring advisory services to the middle market. We offer integrated, multi-product and sector-focused services by pairing highly experienced C-level executives with specialist investment bankers. We aspire to be the trusted advisor of choice to our clients including corporations and institutional investors.

Securities offered through Hollister Associates, LLC, Member FINRA & SIPC.

G2 Capital Advisors, LLC and Hollister Associates, LLC are separate and unaffiliated entities. This does not constitute an offer to buy or sell securities.

CONTACTS ON THIS DEAL:

Jeffrey Varsalone, Managing Director, Restructuring: T: 516.410.0615

E: [email protected]

Konstantin A. Danilov: Vice President, Restructuring: T: 413.841.2717

E: [email protected]

Zach Talotta: Associate, Restructuring: T: 802.745.9291

E: [email protected]