G2 Capital Advisors is pleased to present its Technology & Business Services (“T&BS”) industry update for Q3 2022, providing commentary and analysis on M&A and market trends within the Technology & Business Services sectors and sub-sectors.

The US economic outlook remains uncertain with a general negative sentiment. While supply chain issues are easing, the hiring and job markets remain strong, and consumer spending while slowing is not plummeting, The Conference Board forecasts that economic weakness will intensify and spread more broadly over the coming months driven by inflation and a hawkish Federal Reserve stepping in to aggressively increase the federal funds rate. The Federal Reserve typically walks rates up slowly because they work with a lag, but one that can be powerful. The current rate of increases has them moving more quickly to offset the lag which is a delicate balance. The Federal Reserve’s rate increases represent the fastest tightening since the 1980s when they ultimately raised rates to nearly 20%, sending unemployment to greater than 10%.

The impact on the T&BS M&A market is largely just emerging. We are seeing a slowdown in response increasing costs of leverage and the general uncertainty in the market as well as a marked increase in scrutiny of fit and during diligence. Additionally, many private equity firms were able to return capital to investors from strong exits over the last couple of years, taking the pressure off near term exits. However, quality deals are getting done and 2022 volume is expected to be up from pre-pandemic levels.

Several sectors in particular have seen increased deal volume generated by significant tailwinds. Cybersecurity software and services deals have received interest and attention driven by the ongoing diplomatic tensions between the US and Russia created by Russia’s invasion of Ukraine earlier in the year, as well as the continued fraying of relations with China in response to a host of factors. There has been a similar boom in IT consulting services sector, as companies continue to need highly-specialized, knowledgeable consultants to help them adapt to the ever-changing technology landscape and offset a tight skilled labor force.

G2 Capital Advisors is pleased to present its Consumer & Retail industry update for Q3 2022, providing commentary and analysis on M&A and market trends within the Consumer & Retail sectors.

The world’s largest fast-moving consumer goods companies saw robust growth following the global pandemic, and exhibited resilience in the wake of supply chain constraints and the sharp rise in inflation. In fact, the sector not only survived – it thrived, with average sales exceeding pre-pandemic levels. That said, as sentiment has coalesced around a near-certain downturn, performance is not surprisingly bifurcating between staples and discretionary goods, with prospects for the latter turning sharply.

High inflation, supply chain issues, and increasing recession worries are all factors pressuring the consumer discretionary sector, which already faces the greatest sensitivity to economic cycles. In Q3 2022, discretionary goods companies saw increases in two risk criteria – lowered corporate guidance and greater short interest. Companies in the sector that lowered guidance doubled vs Q2 and increased ten-fold vs Q1, with short interest surpassing all other industries.

Consumer staples, on the other hand, held up better than the broader market, consistent with prior downturns. While the S&P tumbled 25% through Q3, consumer staples stocks fell less than half that, playing their traditionally defensive role. Nonetheless, consumers are now choosing what and where to buy differently, as the pandemic shifted a growing portion of food sales online. Moreover, while many brands enjoy pricing power over private label products, they are nonetheless vulnerable to premium house brands from the likes of Whole Foods and Trader Joe’s.

After years of grappling with the rise of online shopping, brick-and-mortar retailers are posting some of their best results, with retail vacancies at a 15-year low and plans for expansion underway as consumers continue to venture out post-pandemic. In fact, sale growth among physical stores is outpacing that of e-commerce, as the pandemic forced companies to expand and better integrate their omni-channel offerings. While still vulnerable, the retail industry nonetheless appears better-positioned than in prior downturns.

G2 Capital Advisors is pleased to present its Industrials & Manufacturing industry update for Q3 2022, providing commentary and analysis on M&A and market trends within the Industrials & Manufacturing sectors.

A historic, $1.2T of funding has been approved to invest in aging infrastructure nationwide through the Infrastructure Investment and Jobs Act (“IIJA”), coupled with additional investment of $52B through the CHIPS Act and $700B through the Inflation Reduction Act. Construction services firms have been buoyed by the news of the injections, promising years of bumper backlogs and a reliable end customer in the U.S. government. Unfortunately, new investment can’t conjure up a much-needed base of skilled laborers, as the war for talent rages on. Only 80% of the 1MM construction workers who lost their jobs at the beginning of the pandemic have returned, in the face of an estimated 1MM additional workers required in the near term to keep up with high demand. Firms have been forced into bidding wars and are providing more clearly defined career trajectories to attract new workers. As the U.S. hovers over a recessionary state, pressure on wage growth should ease more broadly, but will likely remain an acute issue for the construction services industry as demand is supported by government policy. With spending under the infrastructure law expected to peak in 2027-28, the labor strain is set to become a longer term, structural issue.

The $700B Inflation Reduction Act includes a rejuvenated solar power incentive, increasing the existing tax rebate from 26% to 30% for a period of ten years through 2032. Originally scheduled to phase out between 2020 and 2023, the reboot will be partially financed by a 15% alternative minimum tax on some large U.S. corporations and a 1% excise tax on certain corporate share repurchases. The Biden administration aims to further increase investment and development of renewable energy alternatives, providing a significant boon to developers and investors. This backdrop of robust demand has allowed firms to pass inflationary pressures on to end customers, offsetting the impact on their businesses.

While demand for the construction services and renewable energies sectors will remain robust, supported by extraordinary government funding, industry players will need to combat persistent labor shortages likely to endure through a forecasted recession.

G2 has had an exceptional start to the year, actively supporting over 95 engagements across four industries, serving investment banking and restructuring clients. The firm has made significant investments to expand our leadership functions across the organization with the addition of:

- Brian Steffens – Managing Director, Buy-Side Advisory

- Brian Schofield – Managing Director, Head of Capital Markets

- Jim Cotter – Managing Director, Industrials & Manufacturing

- Jereme LeBlanc – Director, Buy-Side Advisory

As we carry our momentum to the back half of 2022, G2 maintains a steadfast commitment to meeting the evolving needs of our clients across all stages of the business lifecycle. Whether executing strategic growth through M&A or supporting businesses troubled by unsustainable capital structures or challenging industry or operating conditions, G2 is your partner from beginning to end.

CLOSED TRANSACTIONS:

|  |  |  |

|  |  |  |

|

NOTABLE ENGAGEMENTS:

|  |  |  |

|  |  |  |

PERSPECTIVES FROM LEADERSHIP

|  |

|  |

|  |

|  |

G2 Capital Advisors, LLC (“G2”), a leading full-service investment bank and restructuring advisory firm, announced today that Jim Cotter has been hired as a Managing Director on the Industrials & Manufacturing M&A Team, reinforcing the firm’s coverage in industrial technology.

“With more than 25 years of experience in industrials investment banking, Jim’s hiring underscores G2’s commitment to investing in top talent as we continue to grow our platform,” said Matt Konkle, President of G2 Capital Advisors. “In addition to his deep expertise in Industrials, Jim has also worked to source and execute transactions within the Media, Entertainment, Telecommunications, Transportation, and Gaming industries.”

Cotter joins G2 having most recently served as a Managing Director at SunTrust Robinson Humphry for over a decade, where he was the Co-Head of their Industrials M&A group. During his tenure, Jim advised scores of clients across multiple sectors leading efforts to execute strategic transactions for various public and private companies. Before SunTrust, Jim held senior advisory roles at JPMorgan, Jeffries, and CIT Capital. Jim’s advisory experience covers healthy growth company engagements and special situations.

“As we continue to invest and grow our presence in the industrials sector, we’re delighted to welcome Jim, who brings extensive experience across the Industrials and Communications sub-sectors and a proven track record in mergers and acquisitions, strategic corporate development, and special situations,” said Victoria Arrigoni, Head of Industrials & Manufacturing M&A, “With this hire the G2 Industrials & Manufacturing team continues to expand our transaction capabilities and further build on our mission to help clients achieve their strategic and financial goals.”

“G2’s platform is ideally positioned at the forefront of investment banking and restructuring advisory services to the industrials & manufacturing industry. I am thrilled to join the practice and look forward to partnering with the exceptional team assembled under Victoria Arrigoni’s leadership,” said Jim Cotter, Managing Director.

G2 Capital Advisors’ Industrials & Manufacturing team has significant M&A and capital markets experience, which brings deep and relevant knowledge and insight to clients. The firm offers comprehensive and complimentary advisory capabilities through industry experts and M&A bankers that bring expertise across subsectors, geographies, and deal structures.

To learn more about G2’s Industrials & Manufacturing investment banking practice, visit:https://g2capitaladvisors.com/industry-expertise/industrials-manufacturing/

MEDIA CONTACT:

Jennifer Johnson

VP – Head of Marketing

978-204.8050

[email protected]

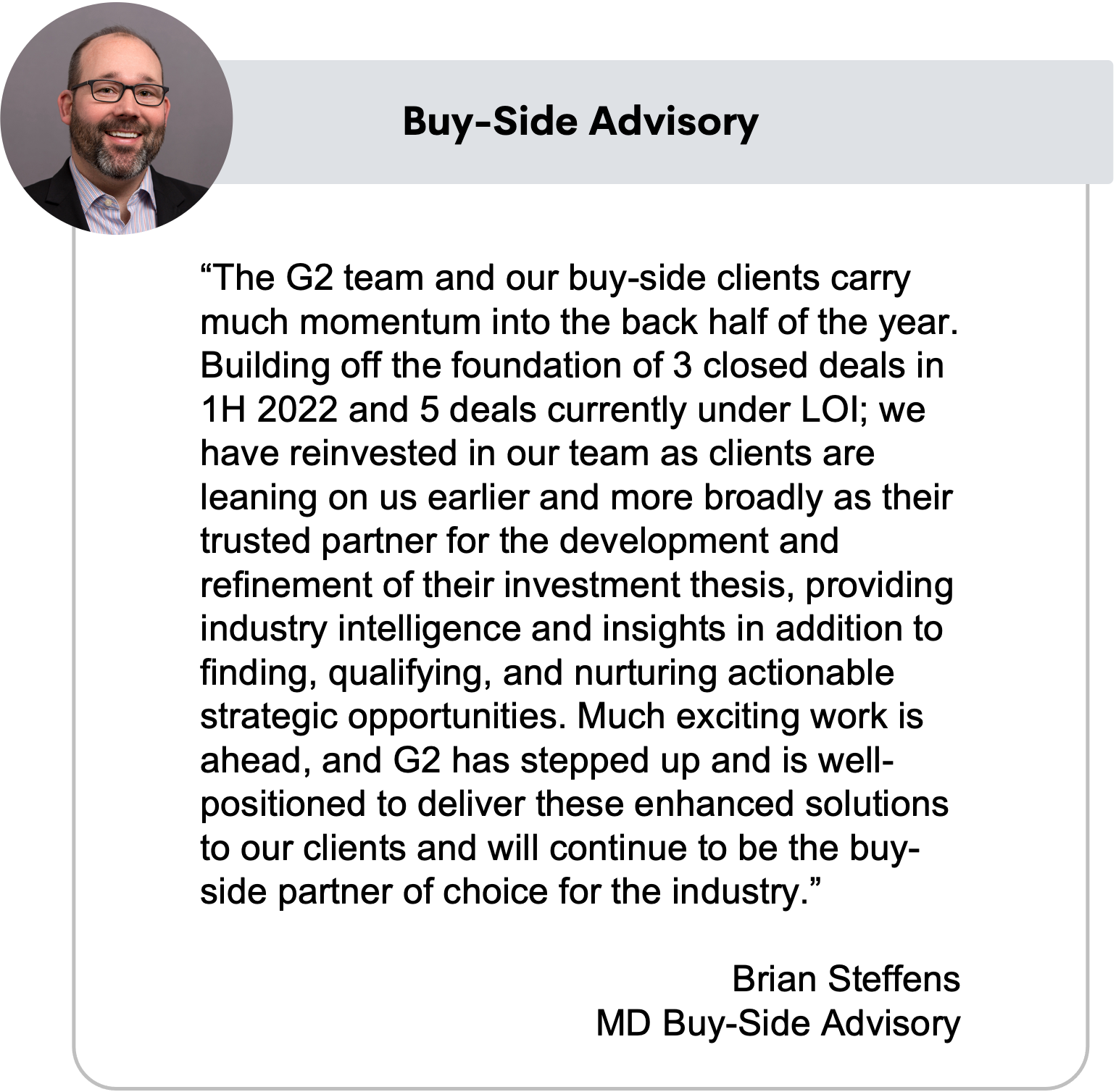

BOSTON, MA – G2 Capital Advisors, LLC (“G2”), a leading full-service investment bank and restructuring advisory firm, has hired Brian Steffens and Jereme LeBlanc to join the Buy-Side M&A advisory practice offering clients support and assistance in defining and executing thoughtfully curated acquisition strategies. With 40+ years of combined industry-focused advisory experience, Steffens and LeBlanc will work collaboratively to manage G2’s buy-side transaction support for private equity and strategic buyers.

“The investment in additional buy-side leadership is core to G2’s focus on delivering valuable industry, market, and strategic advice to our clients,” said Matt Konkle, President of G2. “The buy-side platform significantly enhances G2’s trusted advisory approach, assisting clients to drive growth, maximize value creation, and achieve their strategic objectives.”

The expansion of G2’s Buy-Side M&A team represents a significant opportunity for the firm to support over two dozen active buy-side clients pursuing inorganic growth. In 2021, G2’s grew the buy-side practice substantially, advising 30+ clients and closing eight buy-side transactions.

Brian Steffens joins as Managing Director of G2’s Buy-Side M&A advisory practice. In addition to over 10 years of M&A execution experience covering a range of transactions from buy-side and sell-side to strategic development for large corporate and middle-market clients, Brian previously held financial, operational, and business development roles for portfolio companies as well as leading his own consulting firm focused on value enhancement and growth pre-liquidity event for privately held business owners. He began his career working with the Big 4 accounting firms of PriceWaterhouseCoopers, LLP and Deloitte, LLP. Before joining G2, Steffens was an MD at TruSight, LLC, where he led projects supporting growth strategy objectives for buy-side clients. Over the course of his career Brian has executed inorganic strategy development, target screening, buy-side diligence, and post-merger integration on transactions worth more than $400 MM cumulatively.

Jereme LeBlanc joins as Director, Buy-Side Advisory. LeBlanc brings over 20 years of experience as an M&A advisor and software industry executive. Jereme works exclusively on G2’s buy-side M&A team – specializing in enterprise software and tech-enabled services. Jereme was formerly with Citigroup’s Investment Banking division in New York – and later a Partner at TM Capital, where he led M&A advisory engagements in the enterprise software and IT services sectors. Jereme has successfully executed over 50 transactions worth more than $2.0 billion cumulatively. Jereme spent nine years as a fractional executive in the B2B software industry spearheading corporate development for middle market vendors.

“We are excited to have Brian and Jereme joining our accomplished Buy-Side Advisory practice,” said Ben Wright, Chief Operating Officer at G2 Capital Advisors. “Together, Steffens and LeBlanc bring an exceptional track record supporting high-growth, mission-focused companies, and private equity groups to successfully execute acquisition strategies. Their respective skill sets, and deep investment banking experience make this pair an exceptional addition to our growing practice.”

G2 Capital Advisors offers M&A advisory services, including sell-side and buy-side advisory, capital markets, operational and financial restructuring, and related strategic advisory services to complement a client’s growth plan. With a distinguished track record of advising on nearly $4 billion in closed M&A transactions, providing integrated investment banking services for high-growth companies in the Consumer & Retail, Industrials & Manufacturing, Technology & Business Services, and Transportation & Logistics industries.

While the economic outlook for middle market companies is mixed as we move into 2023, there are still opportunities for growth and success. By being strategic and focused on operational efficiency, cost optimization, and alternative financing options, middle-market companies can navigate these challenges and emerge stronger on the other side.

The rising-rate environment will have an enormous impact on the middle market. Buyers will be more selective and diligent in the companies they acquire, and available liquidity and deal flow will likely decline. Floating-rate debt issuers are especially vulnerable today—particularly those with heavy interest burdens, limited free cash flow, and near-term maturities.

Brian Schofield, MD, Head of Capital Markets, G2 Capital Advisors

The tightening monetary policy, declining GDP growth, and lower public and private valuations will see an impact on middle-market companies in the coming months. With the concern of inflation, the economy slowing down and more, this is what we can expect to see from the middle market:

- Selective and diligent buyers

- Declining deal flow and available liquidity

- Vulnerability among companies

- Covenant-lite loans may assuage default concerns

- Evolutions of investors’ ties with “storied” credits

Our G2 team provides a unique platform, combining deep operational industry experience with capital markets product expertise to meet client growth goals and special situations.

Learn more about our capital marketing advisory.

Capital market analysis & backdrop

Increase in inflation rate remains a crucial concern: After months of claiming inflation was “transitory,” the U.S. Federal Reserve (the Fed) has found itself behind the curve, fighting the highest inflation rate in four decades. The Consumer Price Index (CPI) increased 8.5% for the 12 months ended March 2022, following a year-over-year rise of 7.9% as of February 2022.

The Fed is aggressively tightening monetary policy: The Fed is hiking interest rates—its most aggressive pace of policy tightening since the early 2000s. The Fed voted to raise interest rates by 25 bps in March and 50 bps in May and anticipates an additional 50 bps of hikes during its next two meetings. In addition, the Fed has begun to shrink its $9 trillion balance sheet. Meanwhile, the 10-year Treasury rate is hovering around 3.0%, its highest level since November 2018.

Declining growth as economy is slowing down: U.S. GDP growth fell to 1.4% in the first quarter. However, it was affected by certain factors that should ease throughout the year, including spiking COVID cases and slowing inventory growth. The Fed must balance tightening activity with the risk of tipping the U.S. economy into a recession.

Public markets have been hit hard: Rising interest rates, inflationary pressures, and geopolitical instability have resulted in a public market rout since the beginning of the year. While technology companies and other growth investments have seen the most significant impact, the sell-off has been broad-based and is spilling into the private markets, as further discussed below.

What does this mean for the middle market?

Expect buyers to become more selective and diligent: Valuations in the public markets tend to have a gravitational pull on private transactions. We expect buyers in the middle market to dig in further during due diligence and be highly selective in the companies they seek to acquire.

Available liquidity and deal flow will likely decline: Demand for middle-market loans may exhibit volatility in the second of 2022 as it did in the second quarter of 2020 when deal flow slowed significantly due to uncertainty surrounding the pandemic. Increased borrowing costs will render opportunistic financings less attractive and likely result in muted loan volume for the balance of 2022.

Some companies are more vulnerable than others: Due to the prevalence of floating-rate, debt-heavy capital structures, debt-bearing middle market businesses and loan issuers are more vulnerable than their larger corporate counterparts. Especially vulnerable are companies with limited free cash flow, heavy interest burdens, and near-term maturities that will need to be refinanced at higher interest rates.

Covenant-lite loans may assuage default concerns: A heavy mix of covenant-lite loans, which weaken creditor protections, may help stave off defaults. When debt agreements include maintenance covenants, improved operating performance can mitigate the effects of higher interest rates as monetary policy continues to tighten.

Investors’ willingness to lean in on “storied” credits will evolve: After massive deal activity in late 2021, deal flow has decreased in early 2022, and investors have been more willing to consider complex credits this year. But we expect investor demand to pull back from storied credits as the forward calendar continues to build and scrutiny from lenders increases due to current headwinds.

Market volatility is high, and interest rates are projected to rise. For middle market companies looking to raise capital, now is an opportune time to leverage the expertise of a seasoned capital markets team to navigate the complex market environment and provide greater certainty of execution.”

Brian Schofield, MD, Head of Capital Markets, G2 Capital Advisors

How do these trends affect you?

Our capital markets team would welcome the opportunity to share our perspectives on today’s dynamic capital markets environment and how it affects your specific situation. We have deep experience providing strategic capital markets advice to middle market companies, and we pride ourselves on making the deal experience as efficient as possible for management teams and owners. Contact us to start a conversation today and begin working towards your capital market goals.

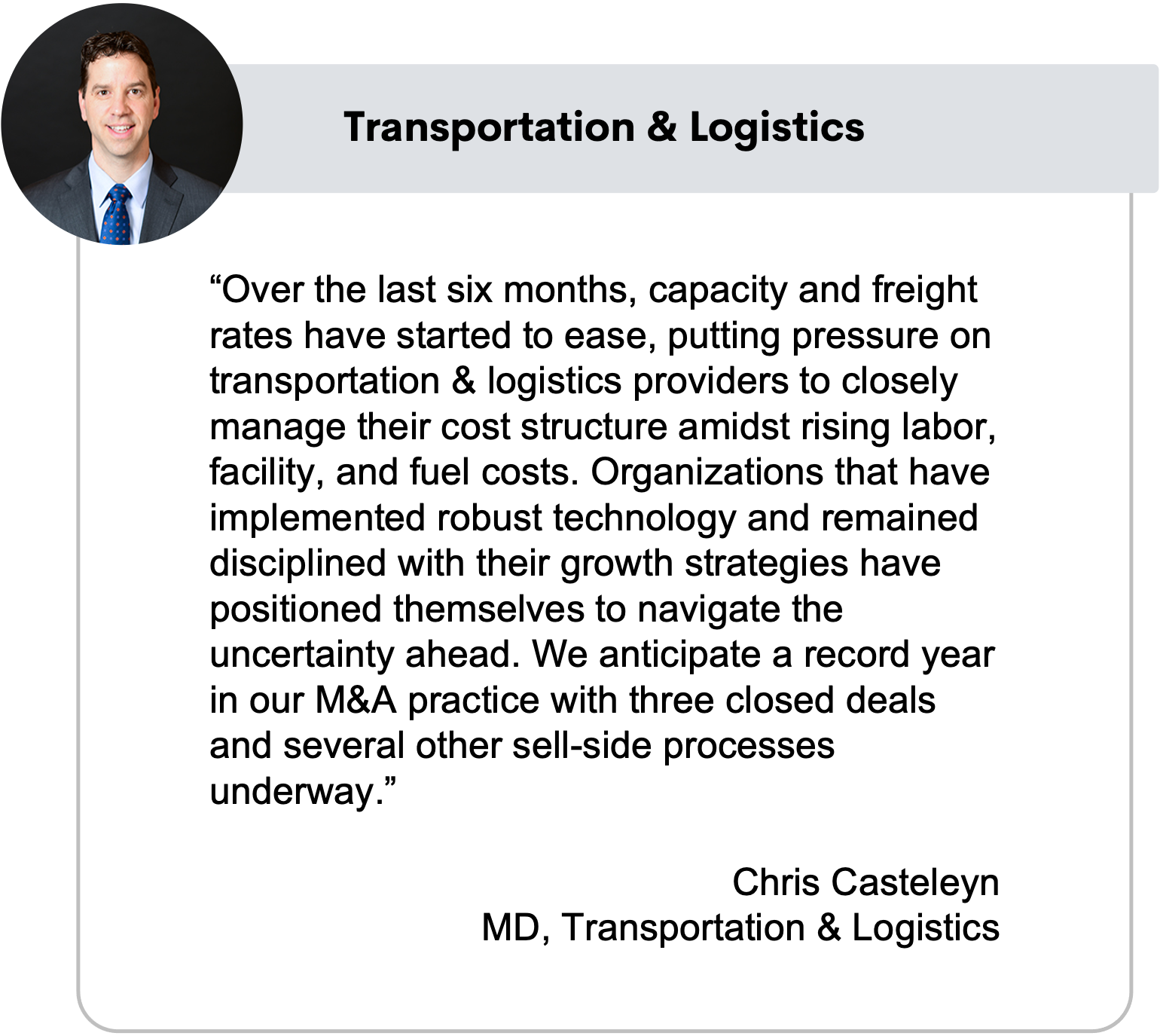

Global supply chain challenges, including port congestion, capacity shortages, increasing ocean rates and ongoing pandemic-related disruptions continue to impact shippers. In response, providers are seeking to strengthen their customer focus by providing a more integrated distribution network, while also increasing their share of customers’ transportation spend across the supply chain.

Submit the form below to view G2’s Transportation & Logistics industry update for Q1 2022, providing commentary and analysis on M&A and market trends within the sector.

G2 Capital Advisors, LLC (“G2”), a leading full-service investment bank and restructuring advisory firm, announced today that Brian Schofield joined as Managing Director, Head of Capital Markets. In this role, Schofield will lead the firm’s capital markets platform with a focus on originating, structuring, and executing debt- and equity-financings in service of private equity firms and middle-market businesses. Schofield will be based out of the Los Angeles area and brings over 15 years of investment banking experience to the position.

“We are pleased to welcome Brian to the G2 team. His experience, knowledge, and proven track record of successfully navigating the complexity of today’s capital markets will serve as an integral aspect of G2’s growth,” said Ben Wright, Chief Operating Officer at G2 Capital Advisors.

Prior to joining G2, Schofield served as a Managing Director at Capstone Partners where he helped lead the Debt Advisory Group. During his time at Capstone, Schofield led capital markets transactions across multiple sectors including environmental services, business services, mining, technology, consumer, and marketing services, amongst others.

Before joining Capstone Partners, Brian was Co-Founder and Partner of Lampert Advisors, a New York-based debt advisory firm. At Lampert he advised middle-market companies and financial sponsors on over $2.5 billion in completed transactions, including acquisition financings, dividend recapitalizations, and restructurings, as well as several buy-side and sell-side M&A transactions.

“I am thrilled to join the team at G2 during a time of such organic growth and expansion. Market demand for capital markets advisory services has never been stronger and we’re committed to making G2 the go-to investment bank for private equity sponsors and business owners seeking to raise debt or equity capital,” said Brian Schofield, Managing Director, Head of Capital Markets.

G2 Capital Advisors offers M&A advisory services, including sell-side and buy-side advisory capital markets, operational and financial restructuring, and related strategic advisory services to complement a client’s growth plan. With a distinguished track record of advising on nearly $4 billion in closed M&A transactions, providing integrated investment banking services for high-growth companies in the Consumer & Retail, Industrials & Manufacturing, Technology & Business Services, and Transportation & Logistics industries.

Cyberattacks: A potent reminder of technological vulnerabilities in the age of automation.

High profile cyberattacks are a potent reminder of growing technological vulnerabilities as manufacturers implement higher levels of automation. Adoption of “Industry 4.0” technology infrastructure is increasing the attack surface to include legacy systems not designed to defend against today’s sophisticated cyber criminal or rogue nation. Ransomware can trigger financial losses, but disruption to production and supply chains can cause harm beyond the initial shake-down. Breaches such as the Colonial Pipeline and SolarWinds attacks grab headlines and underscore the need to defend operations and silo production networks from companies’ external facing business networks. In response, manufacturers should audit not only their existing cyber defenses, but also the resiliency of their operations in the event of a cyber attack.

Cybersecurity plays a vital role in M&A strategy and execution. Firms considering a transaction should understand risks present in the form of data leaks, ransomware, and opportunities for malicious actors to use a transaction as a way to break into an acquiring company. According to IBM, more than half of companies wait until due diligence is completed to perform cybersecurity assessments. Considerations surrounding data privacy regulations, mandatory disclosure laws, and the risk of business interruption should be a priority for sellers and acquirors from the early stages of the transaction process.